In August, America added nearly 1.4 million new jobs according to the Bureau of Labor Statistics monthly Employment Situation Report, in line with the consensus forecast. The unemployment rate fell by 1.8 percentage points to 8.4 percent, the second largest decline on record. The August jobs report confirms that the strong recovery continues.

Just a few months ago, America had an unemployment rate of 3.5 percent—the lowest rate in 50 years—before jumping to a peak of 14.7 percent in April due to devastation wrought by COVID-19. But between April and August, the unemployment rate fell by 6.3 percentage points to 8.4 percent. For perspective, following the Great Recession of 2008-09, it took nearly a decade for the unemployment rate to fall by 6.3 percentage points. President Trump’s economy accomplished this in just four months.

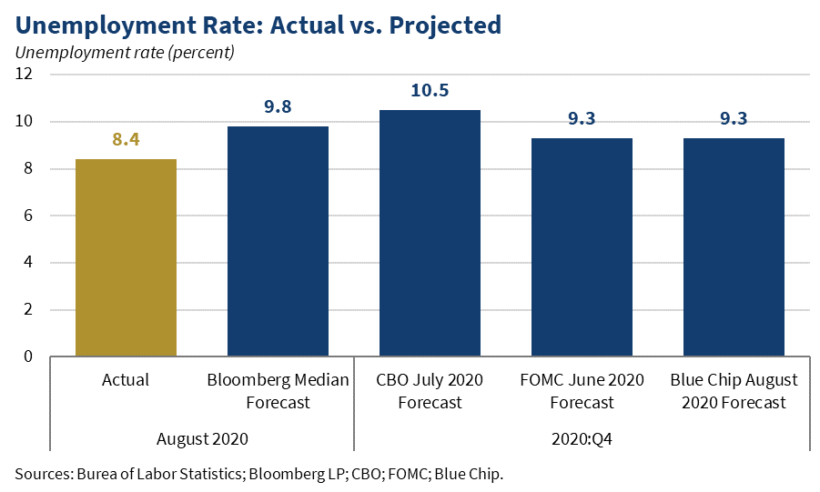

Under this Administration, America is on track to witness the fastest labor market recovery from any economic crisis in history. For four months, the employment report has met or exceeded expectations. In fact, the labor market in August performed better than what most major forecasts projected would occur by year’s end. In July, the Congressional Budget Office (CBO) projected a 10.5 percent unemployment rate in the fourth quarter while both Blue Chip and the Federal Open Market Committee (FOMC) projected unemployment rates of 9.3 percent in the fourth quarter.

As the economy recovers, however, the path to full employment becomes tougher. In April, nearly four out of five jobs lost could be attributed to temporary layoffs, reflecting efforts by Congress and the Administration to keep workers attached to their employers. Four months later, it is apparent why an expedient recovery is vital. The number of temporary layoffs has dropped to just 50 percent as 80 percent of small businesses are now open relative to their pre-COVID-19 levels. Nonetheless, a point of strength in this report lies in the progress we have made since April. At its peak, temporary layoffs hit over 18 million. Since then, temporary layoffs have decreased to just 6 million, a recovery of nearly 67 percent.

The report also shows how this bridge is particularly important for low-income and minority workers who have been hit hardest by the job losses that occurred in March and April. In August, Black American employment increased by 367,000, while employment for Hispanic Americans increased by 1 million, and gains for women increased by 1.5 million. Exemplifying the strong recovery for minority groups, since April, Black American employment has increased by nearly 1.3 million while flows into the labor force have also increased by 663,000.

Those without a high school diploma experienced a 2.8 percentage point decrease in unemployment to a level of 12.6 percent, while those with only a high school diploma are now at an unemployment rate of 9.8 percent after experiencing a 1.0 percentage point decrease in August.

Just a few months ago, America faced an economic shock unlike any other. But in the face of adversity, Americans yet again showed that they will never settle for anything less than great. In July, the unemployment rate was 10.2 percent—0.2 percentage points higher than the peak unemployment rate during the Great Recession in October 2009. It took over two years at that time to achieve an unemployment rate of 8.4 percent, something Americans have now achieved in one month.

With nearly half of the job losses from March and April recovered by August, this report shows that the economic comeback is underway and going strong.